Indirect rates are essential for pricing federal contracts under GSA schedules. They allocate shared costs like rent, HR, and IT across multiple contracts, ensuring compliance and profitability. Missteps in calculating these rates can lead to underpricing, which cuts into profits, or overpricing, making bids less competitive.

Key takeaways:

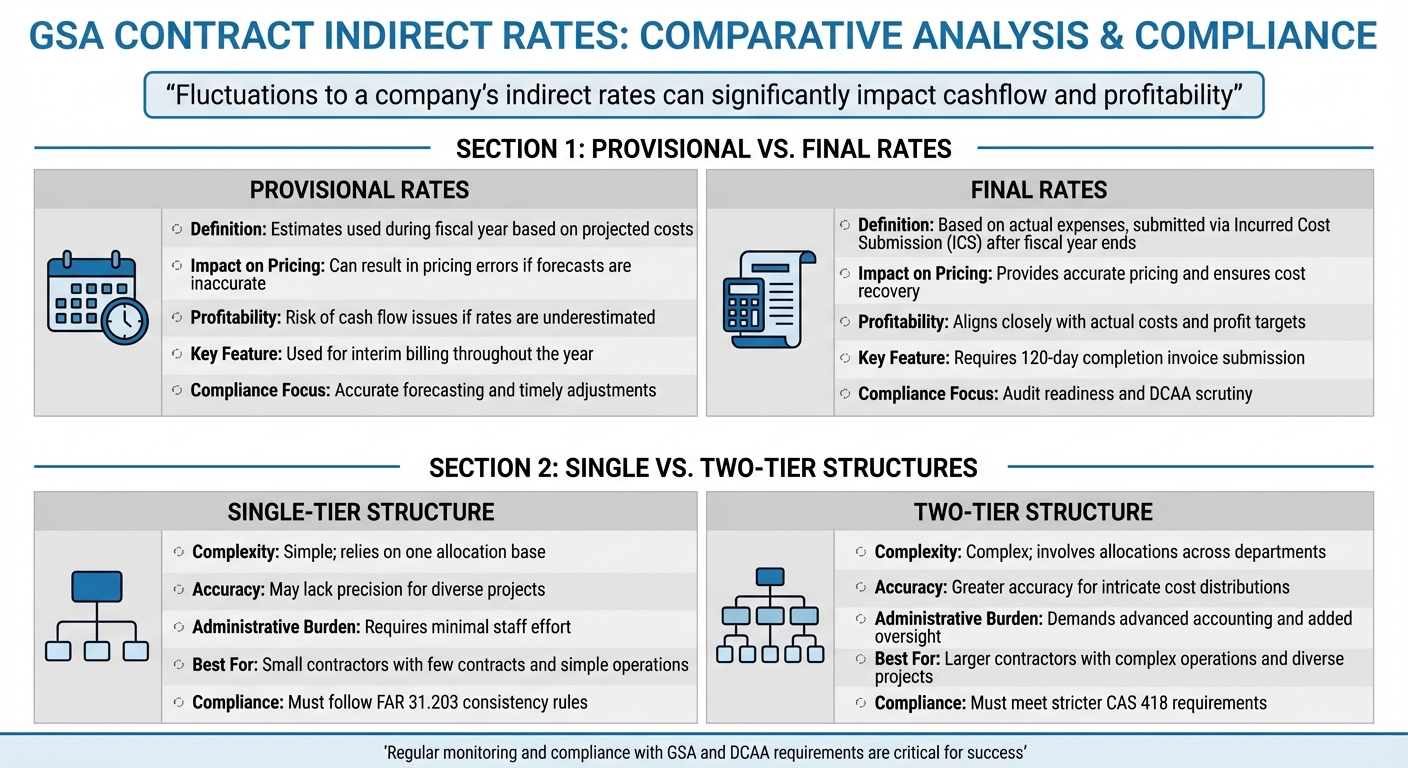

- Provisional Rates: Estimates used during the fiscal year. If inaccurate, they can cause cash flow issues or overbilling.

- Final Rates: Based on actual expenses and submitted via an Incurred Cost Submission (ICS) after the fiscal year ends.

- Single vs. Two-Tier Structures: Single-tier is simpler but less precise, while two-tier provides better cost allocation for complex operations.

Regular monitoring, accurate forecasting, and compliance with GSA and DCAA requirements are critical for success. Small contractors often start with single-tier systems, while larger businesses benefit from two-tier structures for precise cost tracking. Misalignment between provisional and final rates can lead to financial risks, making adjustments during the year vital.

How to Price Your Labor: Indirect Rates and Cost Structures (Government Contracting)

1. Provisional vs. Final Indirect Rates

Getting your rate calculations right is critical when it comes to securing and maintaining competitive GSA contracts. Let’s break down the differences between provisional and final indirect rates and why they matter.

Calculation Methods

Provisional indirect rates act as estimates you provide at the beginning of your fiscal year. These rates, based on your projected overhead, fringe, and G&A expenses, allow you to invoice the government during the contract period, keeping your cash flow steady.

On the other hand, final indirect rates are calculated after your fiscal year ends, using the actual costs you incurred. This process involves submitting an Incurred Cost Submission (ICS), which reconciles what you billed using provisional rates against your actual expenses. If your provisional rates were too high, you’ll owe the government the excess. If they were too low, you’ll face a shortfall and miss out on recovering your full costs.

"Provisional rates, sometimes referred to as billing rates, are used throughout the year to estimate indirect cost recovery. These rates are typically based on budgeted or forecasted costs." – Michael Diener, CPA, Diener & Associates

The reconciliation process isn’t optional. Once your final rates are settled, you have 120 days to submit a completion invoice reflecting the corrected amounts. If you miss this deadline, the Contracting Officer could unilaterally decide what you’re owed – a risk no contractor wants to take.

These methods don’t just affect your accounting – they directly shape your GSA pricing strategy.

Impact on GSA Pricing

Provisional rates require careful calibration. Set them too low, and you’ll underbill, straining your cash flow and leaving money unclaimed. Set them too high, and you’ll end up overbilling, forcing you to refund the government after reconciliation. Neither scenario is ideal for staying competitive in the GSA market.

Your pricing accuracy hinges on how closely your provisional rates align with your actual costs. But here’s the tricky part: if your cost structure changes mid-year – like hiring new staff or moving to a more expensive office – your provisional rates can quickly become outdated. Thankfully, you’re not stuck. You can request an interim adjustment from your Administrative Contracting Officer (ACO) to reflect these changes. This keeps your billing accurate and protects your cash flow.

Contractors who use specialized rate strategy services report bid-price accuracy within 2%. That level of precision can make all the difference when competing for federal contracts where every dollar counts.

These considerations aren’t just about pricing – they also impact your cash flow, profit margins, and compliance efforts.

Profitability and Compliance

Staying on top of rate variances is key. Regular monitoring – monthly or quarterly – helps you detect discrepancies early and adjust your billing as needed. This proactive approach minimizes financial surprises.

"The difference between provisional and final rates can have significant financial implications, particularly in cases where actual costs vary materially from initial forecasts." – Michael Diener, CPA

Compliance challenges differ depending on whether you’re dealing with provisional or final rates. For provisional rates, the focus is on accurate forecasting and timely adjustments. When it comes to final rates, the priority shifts to audit readiness. Your ICS needs to hold up under the scrutiny of the Defense Contract Audit Agency (DCAA). A well-organized Chart of Accounts (COA) that categorizes costs into proper pools – like fringe, overhead, and G&A – can streamline this process and lower your audit risks.

Understanding these nuances is essential for aligning your pricing strategy with compliance and profitability goals.

2. Single vs. Two-Tier Indirect Rate Structures

Your choice of indirect rate structure – single-tier or two-tier – has a direct impact on GSA contract pricing and how efficiently you can manage administrative tasks. Just like the decision between provisional and final rates, this choice shapes cost accuracy and your ability to stay competitive in the GSA marketplace.

Calculation Methods

Single-tier structures are straightforward. Here, all your indirect cost pools – like overhead, fringe, and general & administrative expenses – get directly allocated to your final cost objectives (contracts). This simplicity makes it a good fit for small contractors with just a few contracts and uncomplicated operations.

Two-tier structures, on the other hand, involve an extra step. Indirect costs are first allocated to intermediate objectives before being distributed to other pools or final contracts. This method is more common among larger contractors with complex operations. For instance, two-tier structures allow precise tracking of costs across different service areas.

"Small contractors with few contracts may use single-tier indirect rate structures in which the contractor allocates all indirect cost pools immediately to final cost objectives."

– Keith R. Szeliga, Partner, Sheppard Mullin

The main difference lies in precision versus simplicity. A two-tier structure offers more detailed cost tracking, such as creating separate overhead pools for work at government sites versus your own facilities, ensuring costs align more accurately with the benefits received. Meanwhile, single-tier structures prioritize ease of use, making them practical for smaller businesses.

Impact on GSA Pricing

The rate structure you choose doesn’t just affect your internal accounting – it also influences your pricing competitiveness. For contractors performing substantial work at government facilities, a two-tier structure can be a game-changer. By setting up a dedicated "government-site" overhead pool, you can avoid overpricing your bids by excluding costs irrelevant to on-site work. This can make your proposals more attractive and help you secure contracts.

Single-tier structures, while simpler, might lead to over- or under-allocating costs, as they treat all work the same. For smaller firms with standardized operations, the reduced administrative effort might outweigh the slight loss in precision. However, as your business grows and your contracts diversify, the added precision of a two-tier structure could become worth the investment. It’s important to note that two-tier systems demand more advanced accounting tools to maintain compliance with Cost Accounting Standards (CAS) 418, which requires that cost pools remain homogeneous. Regular reviews are crucial to ensure these pools accurately reflect their causal relationships to your contracts.

Profitability and Compliance

The best structure for your business depends on its size and the complexity of your contracts. Many small businesses start with a single-tier setup to keep administrative tasks manageable. As operations expand or contracts become more intricate, transitioning to a two-tier structure can help improve cost allocation and overall profitability.

"Achieving an equitable distribution of costs may require creating separate indirect cost pools for work performed at Government and contractor sites."

– Keith R. Szeliga, Partner, Sheppard Mullin

Compliance is a critical factor regardless of the structure you choose. Single-tier systems need to follow basic consistency rules under FAR 31.203, while two-tier setups must meet stricter requirements under CAS 418. If your cost pools begin to show different causal relationships to contracts, federal regulations might require you to adopt a two-tier structure, even if it adds administrative complexity.

To stay compliant and profitable, regularly review your allocation methods to ensure they align with your evolving business needs. Federal regulations demand fairness in cost distribution, so periodic evaluations are key to avoiding compliance risks and maintaining audit readiness.

Advantages and Disadvantages

Provisional vs Final Indirect Rates and Single vs Two-Tier Rate Structures Comparison

The following tables break down the trade-offs between different indirect rate approaches, shedding light on how each choice affects competitive pricing and profit margins in GSA contracts.

Comparison Table: Provisional vs. Final Rates

| Aspect | Provisional Rates | Final Rates |

|---|---|---|

| Impact on Pricing | Can result in pricing errors if forecasts are inaccurate | Provides accurate pricing and ensures cost recovery |

| Profitability | Risk of cash flow issues if rates are underestimated | Aligns closely with actual costs and profit targets |

"Fluctuations to a company’s indirect rates can significantly impact cashflow and profitability".

Provisional rates introduce risks when estimates fall short, potentially straining cash flow. On the other hand, final rates offer precision by reconciling costs with actual expenses.

Comparison Table: Single vs. Two-Tier Structures

| Aspect | Single-Tier Structure | Two-Tier Structure |

|---|---|---|

| Complexity | Simple; relies on one allocation base | Complex; involves allocations across departments |

| Accuracy | May lack precision for diverse projects | Greater accuracy for intricate cost distributions |

| Administrative Burden | Requires minimal staff effort | Demands advanced accounting and added oversight |

Single-tier structures are straightforward and easy to manage but may not suit varied project needs. Two-tier systems, while more demanding, provide the precision required for managing diverse contract portfolios effectively.

Conclusion

Choosing the right indirect rate structure hinges on your business model and the complexity of your operations. Provisional indirect rates – calculated using forecasted costs – offer flexibility for interim billing. However, if your estimates are off, you risk recovering less than your actual costs. On the other hand, final rates reconcile actual costs but require detailed year-end accounting to ensure accuracy.

For smaller businesses or startups with simple operations and limited outsourcing, a single-tier system is often the best fit. These systems are easier to manage and involve less administrative effort. In contrast, two-tier structures are better suited for more established contractors with diverse projects or significant R&D activities, as they allow for more precise allocation of indirect costs. Regardless of the structure you choose, ongoing monitoring throughout the contract period is essential to ensure clarity and accuracy in cost allocation.

It’s a good practice to compare your provisional and actual costs on a monthly or quarterly basis. If you notice a significant gap between the two, submitting revised provisional rates to the government mid-year might be necessary. As Dave Donley from ReliAscent explains:

"Indirect rates, and their ‘structure,’ are perhaps less important for start-ups with smaller contract and grant values but become very important as a company grows and prospers".

To ensure compliance and accurate pricing, maintain logical cost pools and clear allocation bases. Whether you choose a three-tier model with fringe, overhead, and G&A or stick to a simpler single G&A pool, your ultimate goal should be the same: setting rates that protect your profit margins while staying compliant.

FAQs

How do indirect rates affect my GSA pricing?

Indirect rates play a key role in shaping your GSA pricing by tacking on overhead and administrative expenses to your direct costs. These additions ultimately raise the price you propose to the government. Accurately calculating these rates is crucial – not just for staying competitive in the market but also for meeting federal compliance requirements.

When should I update my provisional rates?

You should plan to update your provisional rates 12 months after your contract is awarded. To stay compliant with GSA and FAR guidelines, make sure there is at least a 30-day gap between any update requests.

Do I need a single-tier or two-tier structure?

When deciding between a single-tier or two-tier indirect rate structure, the right choice largely hinges on your company’s size, operational complexity, and how you need to allocate costs.

A single-tier structure consolidates all indirect costs into one rate. This approach is straightforward and easier to manage, making it a good fit for smaller organizations or those with simpler operations.

On the other hand, a two-tier structure divides these costs into categories like overhead and general and administrative (G&A). This method provides a more detailed allocation, which can be helpful for compliance and tracking purposes. However, it does come with the trade-off of increased administrative effort.

Ultimately, your decision should reflect the complexity of your operations and align with your goals for federal contracting.

Related Blog Posts

- Ultimate Guide to GSA Labor Rate Development

- How Indirect Costs Impact Government Contract Pricing

- How Indirect Costs Impact Government Bids

- Key Indirect Cost Considerations for Bidding