Fringe benefits are a key part of federal contracting and GSA pricing. They include compensation beyond wages, like health insurance, retirement plans, and paid leave. However, not all benefits qualify under GSA rules. This guide explains how fringe benefits impact labor rates, compliance, and pricing for GSA contracts.

Key Takeaways:

- What Counts as Fringe Benefits: Only "bona fide" benefits (offered through enforceable plans) qualify. Mandatory contributions like Social Security are excluded.

- Why They Matter: Fringe benefits affect fully loaded labor rates, which determine your contract pricing and competitiveness.

- Calculation Methods: Common approaches include actual cost, standardized SCLS rates, and burden rates. Each has pros and cons depending on your contract type.

- Compliance: Accurate documentation and adherence to SCLS wage determinations are essential to avoid penalties.

Fringe benefits aren’t just a compliance factor – they influence your ability to attract talent and meet contract requirements. Keep reading to learn how to calculate them, avoid common mistakes, and ensure your GSA pricing aligns with federal standards.

Government Contracting – How To Create Indirect Rates – Win Federal Contracts

How to Calculate Fringe Benefits for GSA Labor Rates

GSA Fringe Benefits Calculation Methods Comparison Chart

Methods for Calculating Fringe Benefits

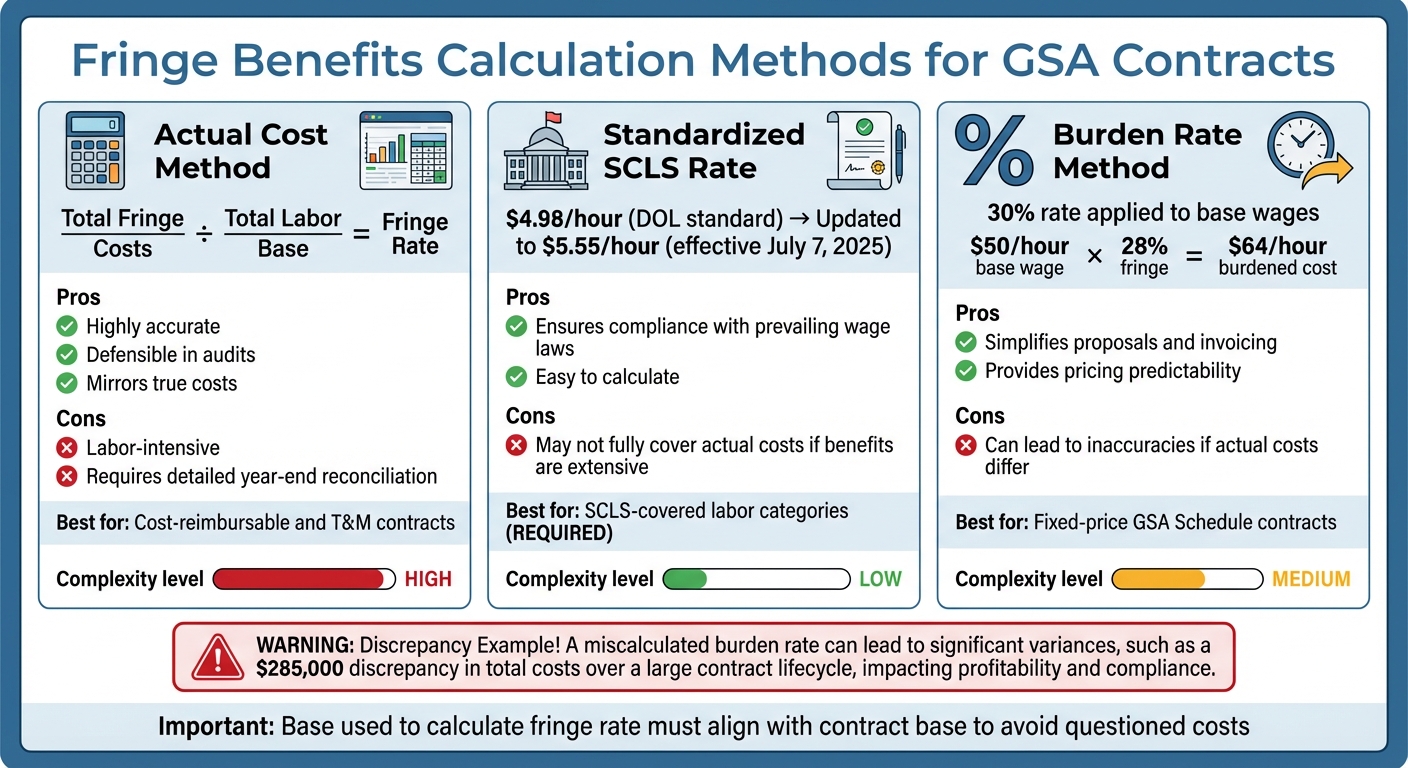

When it comes to calculating fringe benefits, contractors typically rely on one of three approaches. Each method has its strengths and limitations, and the choice often depends on the contract type and the level of detail required.

The actual cost method is straightforward in theory but demands meticulous accounting. Here, you divide total fringe costs by the total labor base, which includes both direct and indirect labor. The formula looks like this: Total Fringe Costs ÷ Total Labor Base = Fringe Rate. This method ensures an accurate reflection of your company’s true costs, but it requires constant updates and detailed record-keeping to stay reliable.

For labor categories covered by Service Contract Labor Standards (SCLS), the standardized SCLS rate comes into play. The Department of Labor sets fixed hourly rates for benefits, such as $4.98 per hour for health and welfare. This method guarantees compliance with statutory requirements but may not align with a contractor’s actual benefit expenses.

Lastly, the burden rate method applies a pre-determined percentage – often based on historical data or industry benchmarks – to wages. For instance, you might use a 30% rate across the board. While this method is simple and efficient for proposals, it can lead to under- or over-recovery if actual costs deviate from the assumed rate.

Adding Fringe Benefits to Fully Loaded Labor Rates

Fringe benefits are treated as an indirect cost and are added to the base wage to calculate a fully loaded labor rate. The process starts with an employee’s base pay, applies the fringe rate to determine the "burdened" labor cost, and then includes additional markups like overhead, general and administrative expenses (G&A), and profit.

For example, if an employee earns $50.00 per hour and the fringe rate is 28%, the burdened labor cost becomes $64.00 per hour before adding overhead, G&A, and profit.

Important to note: The base used to calculate the fringe rate must align with the base applied to contracts. Misalignment can lead to questioned costs, as highlighted by a case where $285,000 in discrepancies arose due to inconsistent allocation.

To better understand how these methods compare, the table below outlines their key features and their relevance in different contract scenarios.

Comparison of Calculation Methods

| Method | Description | Pros | Cons | GSA Applicability |

|---|---|---|---|---|

| Actual Cost | Divides actual fringe expenditures by the labor base. | Highly accurate; defensible in audits; mirrors true costs. | Labor-intensive; requires detailed year-end reconciliation. | Best for cost-reimbursable and T&M contracts. |

| Standardized SCLS Rate | Uses a fixed hourly rate (e.g., $4.98/hr) set by the DOL. | Ensures compliance with prevailing wage laws; easy to calculate. | May not fully cover actual costs if benefits are extensive. | Required for SCLS-covered labor categories. |

| Burden Rate | Applies a fixed percentage to base wages. | Simplifies proposals and invoicing; provides pricing predictability. | Can lead to inaccuracies if actual costs differ. | Common for fixed-price GSA Schedule contracts. |

Service Contract Labor Standards and Fringe Benefits

Understanding SCLS Wage Determinations

The Service Contract Labor Standards (SCLS), previously known as the Service Contract Act, apply to federal service contracts valued over $2,500. These regulations ensure that contractors pay service employees at least the locally prevailing wage rates and fringe benefits established by the U.S. Department of Labor.

Under these rules, wage determinations specify a minimum hourly wage along with separate fringe benefit rates. The U.S. Department of Labor emphasizes this distinction:

"The fringe benefit requirements (usually ‘health and welfare,’ vacation, and holiday benefits) are separate and in addition to the hourly monetary wage requirement under the SCA."

- U.S. Department of Labor

In other words, contractors cannot bypass fringe benefit obligations by offering a higher hourly wage. Both the wage and fringe benefit requirements must be fulfilled independently.

For GSA Multiple Award Schedule contracts, wage determinations are updated annually through solicitation refreshes or mass modifications. However, new rates only take effect after formal incorporation by the Contracting Officer.

Now, let’s explore which labor categories fall under these requirements.

Which Labor Categories Require Fringe Benefits

SCLS applies to service employees delivering nonprofessional services under GSA Multiple Award Schedule contracts. These employees primarily provide services through their labor. However, there are exclusions: SCLS does not cover employees in executive, administrative, or professional roles, nor does it apply to construction contracts under the Davis-Bacon Act, work governed by the Walsh-Healey Public Contracts Act, or services performed outside the United States.

When responding to a Request for Quotation, contractors must identify labor categories subject to SCLS. The GSA eLibrary includes an SCLS matrix in the authorized schedule price list to help pinpoint applicable categories. If a labor classification isn’t included in the wage determination, the conformance process allows contractors to propose suitable wage and benefit rates for the unlisted classification.

With these classifications in mind, let’s review the specifics of health and welfare rate requirements.

SCA Health and Welfare Rates

Health and Welfare (H&W) rates are the most common fringe benefit requirement under SCLS. Starting July 7, 2025, the standard H&W rate is $5.55/hour. For contracts governed by Executive Order 13706, which mandates paid sick leave, the rate is slightly lower at $5.09/hour. In Hawaii, where the Prepaid Healthcare Act is in effect, the rates are $2.42/hour for standard contracts and $1.96/hour for EO 13706 contracts.

These rates apply to all paid hours – vacation, sick leave, and holidays included – up to 40 hours per week and 2,080 hours annually per contract. Contractors can meet this requirement through bona fide fringe benefits, a cash supplement, or a mix of both. If the cost of a benefit plan falls short of the required rate, the contractor must pay the difference as a cash supplement.

To determine which H&W rate applies to your contract, look for FAR clause 52.222-62. If it’s included, the lower EO 13706 rate applies. Noncompliance with SCLS requirements can lead to severe consequences, including a three-year ban from federal contracting.

Compliance and Documentation Requirements

Required Fringe Benefit Documentation

If you’re a GSA contractor, keeping separate records for wages and fringe benefits isn’t just a good practice – it’s a requirement. According to the U.S. Department of Labor:

"A contractor cannot pay a higher monetary wage rate than what is required under the wage determination in order to satisfy its fringe benefit obligation, and must keep accurate records separately showing amounts paid for wages and amounts paid for fringe benefits".

For fringe benefit plans to meet the "bona fide" standard, they must be in writing, legally enforceable, and clearly communicated to employees. Essential documentation includes a fringe pool justification, which explains what costs are included, why they align with FAR Part 31, and provides source records that match your accounting system. Amanda Dunning of Cheryl Jefferson & Associates advises:

"The costs you include in fringe need to be allowable, allocable, and reasonable, and you need to be able to support them with documentation if asked".

Other critical documents include:

- Length of service records: Used to determine vacation eligibility.

- SCLS matrix: Must be part of your authorized schedule price list.

- Approval letters: Required for unfunded self-insured plans from the DOL Administrator.

- Proof of contributions: For funded plans, show that contributions were made irrevocably to an independent trustee or third party.

When calculating hourly cash equivalents, divide the total cost by the actual hours worked. For instance, a $112 monthly health insurance premium divided by 125 hours worked equals $0.90 per hour.

Next, let’s look at what happens when fringe benefit costs change after your contract is awarded.

How to Handle Fringe Benefit Changes After Award

GSA updates SCLS wage determinations, including fringe benefit rates, on an annual basis. These updates typically come through mass modifications tied to solicitation refreshes. To avoid delays, make sure to sign mass modifications within 90 days.

If your fringe costs change, submit a contract modification via eOffer/eMod using the designated template. Review your EPA clause (like GSAR 552.238-120) to ensure compliance, and update your negotiators’ and points-of-contact information in the eMod system.

Now, let’s explore how GSA ensures compliance with fringe benefit requirements.

GSA Compliance Reviews for Fringe Benefits

When GSA conducts compliance reviews, they check that you’re meeting the base rate and fringe benefit obligations outlined in the SCLS wage determination incorporated into your contract. Contractors can meet these requirements either through additional cash wages or bona fide benefit plans. The advantage of bona fide benefit plans? They can reduce payroll tax obligations, including FICA, FUTA, SUTA, and Workers’ Compensation costs.

To prepare for audits, create a detailed reporting guide tailored to the wage determination or Collective Bargaining Agreement that applies to your contract. Regularly reconcile your hours and benefits records to catch any discrepancies early. GSA National underscores the importance of this:

"Determining your SCA contracts’ health and welfare liability, both past and present, is essential to maintaining your long-term viability in the government contracting arena".

Noncompliance isn’t just a slap on the wrist – it can lead to contract terminations, withheld payments, financial penalties, and even debarment from future federal contracts.

Common Mistakes and How to Avoid Them

Avoiding Calculation Errors

Contractors often stumble when written policies don’t align with accounting system accruals. Michael Diener, CPA at Diener & Associates, highlights this issue:

"If a contractor’s handbook states that employees accrue a certain number of paid time off hours per year, but the accounting system allocates a higher amount in cost calculations, the resulting fringe rate will be artificially inflated".

This discrepancy can lead to inflated fringe rates, which skew cost calculations and raise audit concerns.

Another frequent misstep is including unallowable costs – like personal vehicle use or lobbying expenses – in fringe pools. Contractors also err by directly charging paid leave (vacation, sick leave, holidays) to contracts instead of pooling them in the fringe account. This practice distorts labor charges and draws scrutiny during audits.

Additionally, failing to update fringe rates after changes in health insurance premiums, retirement contributions, or adjustments under the Service Contract Act (SCA) is a common error. Fringe pools should reflect current costs, not outdated figures. To ensure accuracy, all paid leave must be coded to fringe accounts in your timekeeping system. Otherwise, the fringe rate numerator may be understated, leading to incorrect cost recovery.

| Common Mistake | Impact | Prevention Strategy |

|---|---|---|

| Including unallowable costs (e.g., alcohol, lobbying) | Audit disallowances and financial penalties | Use FAR Part 31 exclusion checklists |

| Outdated benefit data | Overcharging or lost revenue | Update fringe pools after benefit changes |

| Charging leave directly to contracts | Distorted labor charges and audit findings | Route all paid leave through fringe accounts |

| Policy-system misalignment | Inflated fringe rates | Align policies with accounting records |

Regular reviews and adjustments are key to maintaining accurate fringe benefit calculations.

Maintaining Fringe Benefit Compliance

Once errors are identified, adopting strong compliance measures can prevent them from recurring. Quarterly reviews are crucial for comparing provisional fringe rates to actual year-end results. These reviews help limit retroactive adjustments and ensure billing remains consistent.

During each review, use a checklist to confirm that unallowable costs are excluded, paid leave is routed correctly, and all documentation is in order. Properly configuring your timekeeping system ensures all paid leave is accurately coded to fringe accounts. When Service Contract Labor Standards (SCLS) wage determinations change, adjust contract pricing to reflect only the net change in fringe obligations, avoiding overcharges or undercharges.

Michael Diener emphasizes the importance of avoiding missteps:

"Fringe benefit rates play a direct role in cost recovery and compliance for federal contractors, yet any missteps in their calculation remain one of the most common and avoidable sources of audit findings".

Why Accurate Recordkeeping Matters

Accurate recordkeeping is the foundation of error prevention and compliance. Without it, contractors risk serious repercussions. Fringe rate errors can result in an "inadequate" accounting system designation under DFARS, leading to payment withholds of 5% to 10% of billed amounts. Submitting unallowable costs may also result in penalties equal to the disallowed amount – or double if negligence is determined.

To avoid these risks, maintain original records such as timesheets, benefit invoices, payroll tax filings, and Negotiated Indirect Cost Rate Agreements (NICRAs). Auditors rely on these documents to verify calculations. Submitting clearly unallowable fringe costs can trigger penalties under FAR and U.S. Code Title 10 §3743, and ongoing misreporting could lead to liability under the False Claims Act.

Conclusion

Fringe benefits go beyond being just another detail in your GSA pricing – they play a key role in cost recovery, audit preparation, and staying competitive. Getting the calculations right means aligning allocation and application bases, excluding unallowable costs, and clearly distinguishing between fringe, overhead, and G&A expenses. When these processes falter, the fallout can be significant. For example, a DCAA audit once challenged $285,000 in contract costs because of an incorrect fringe allocation method that resulted in double recovery.

This highlights how crucial it is to allocate fringe benefits accurately. Beyond meeting audit requirements, your fringe rate assumptions send a message to contracting officers about your ability to attract and retain skilled employees while keeping costs stable throughout the contract period.

To safeguard against compliance issues, thorough documentation and consistent oversight are essential. Keep original records, such as timesheets, benefit invoices, payroll tax filings, and NICRAs, to back up your calculations during audits. Conduct quarterly reviews to compare provisional rates with actual results, minimizing the need for retroactive adjustments. Additionally, when Service Contract Act wage determinations change, adjust pricing to account only for the net change in fringe obligations. Failing to meet labor standards can lead to serious consequences, including contract termination, payment withholding, and even being barred from future federal contracts. On the flip side, adopting a compliant fringe benefit allocation method – typically costing $8,000 to $25,000 upfront, with annual maintenance expenses ranging from $3,000 to $8,000 – can protect your business and provide a reliable platform for growth.

In federal contracting, precision in fringe benefit pricing isn’t optional. It can mean the difference between long-term success and costly compliance missteps that could jeopardize your business. For expert help with fringe benefit pricing and ensuring compliance with federal standards, reach out to GSA Focus.

FAQs

What qualifies as “bona fide” employee benefits under GSA rules?

Under GSA rules, bona fide fringe benefits must meet certain criteria to qualify. They need to be a legally enforceable obligation, properly documented in writing, and clearly communicated to employees. These benefits must also be offered through a legitimate benefits plan. Examples include healthcare coverage or retirement plans, but not cash substitutes like direct payments. To comply, the benefits must adhere to specific legal standards.

How do I choose between actual cost, SCLS, and burden rate methods?

When deciding on a method, consider your contract obligations and compliance demands:

- Actual Cost: This approach divides total fringe benefit costs by the payroll base, aligning with contract-specific charging practices.

- SCLS (Service Contract Labor Standards): Relies on GSA-designated wage and fringe rates to meet labor standards requirements.

- Burden Rate: Allocates indirect costs, including fringe benefits, for use in estimating and proposal development.

The priority here is maintaining consistency while adhering to compliance standards.

What records should I keep to pass a fringe benefits compliance review?

To successfully navigate a fringe benefits compliance review, it’s crucial to keep detailed and accurate records. This includes tracking employee hours, documenting allowable benefits, maintaining employee statements, and preparing reconciliation reports. Organized and precise documentation not only ensures compliance but also makes the entire review process much smoother.

Related Blog Posts

- Cost Element Breakdown in GSA Contracts

- Ultimate Guide to GSA Labor Rate Development

- Labor Rate Escalation: What GSA Contractors Need to Know

- How GSA Pricing Impacts Federal Contract Bids