The landscape for GSA price list audits in 2026 has become more stringent and complex, especially for small businesses. Key changes include the mandatory implementation of Transactional Data Reporting (TDR) for all contractors, replacing older frameworks like Commercial Sales Practices (CSP) and the Price Reductions Clause (PRC). This shift demands monthly reporting of detailed transaction data, giving auditors greater visibility into pricing and compliance.

Key Points:

- Increased Audit Scrutiny: Following a February 2026 OIG report exposing price inconsistencies, contractors must now provide detailed pricing justifications for all MAS awards.

- TDR Requirements: Expanded to all contractors under MAS Refresh #31, with monthly reporting deadlines.

- Economic Price Adjustments (EPA): New standards under MAS Refresh #29 require precise documentation and longer approval times.

- Small Business Challenges: Documentation accuracy, pricing clarity, and compliance with dual audit frameworks (CSP vs. TDR) remain significant hurdles.

Staying compliant means maintaining organized records, meeting reporting deadlines, and understanding contract-specific requirements. Small businesses should consider professional support to navigate these changes and avoid potential contract risks.

Key Insights for GSA Schedule Contracting

How Transactional Data Reporting (TDR) Affects Audits

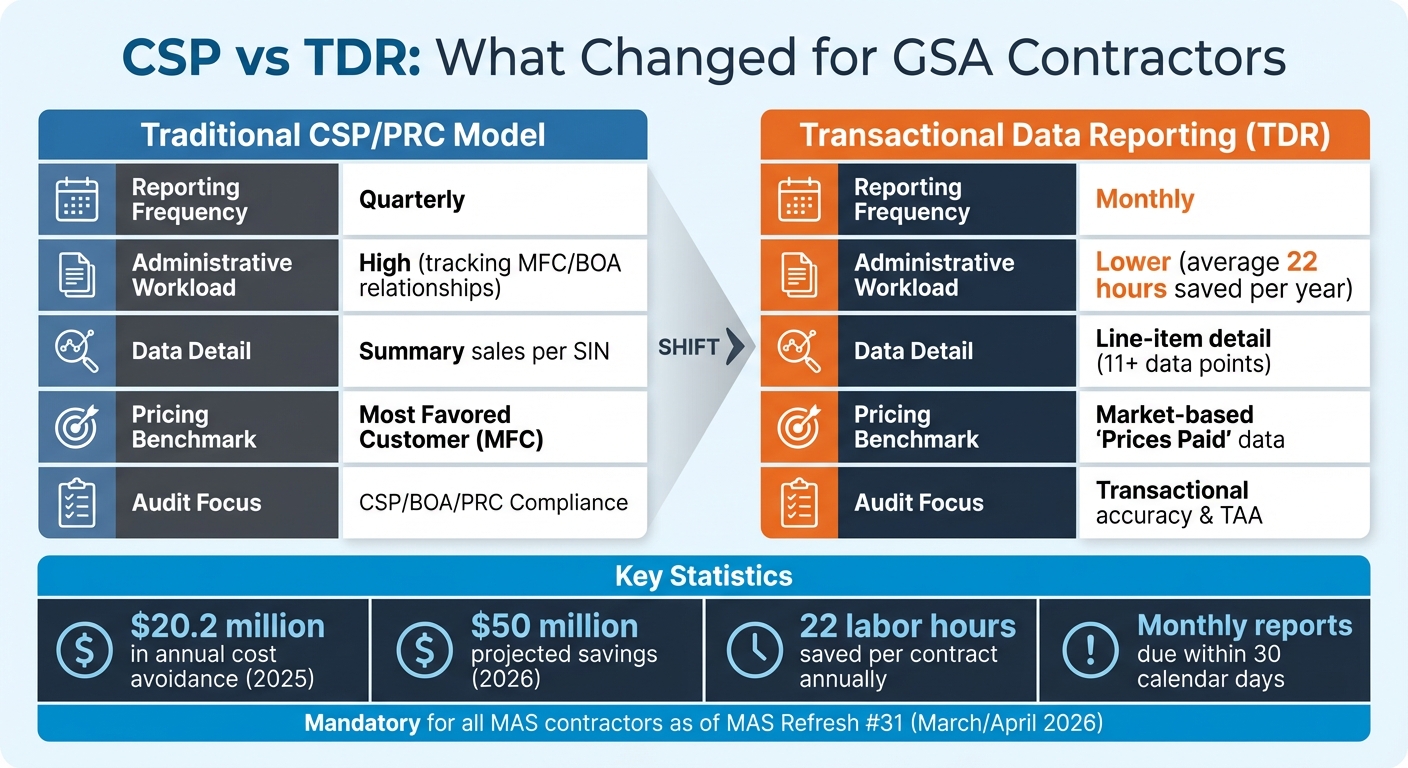

CSP vs TDR Reporting Requirements Comparison for GSA Contractors

Transactional Data Reporting (TDR) has reshaped the way audits are conducted by the General Services Administration (GSA). Starting with MAS Solicitation Refresh #31 in March/April 2026, TDR became a mandatory requirement for all Multiple Award Schedule contractors, replacing the legacy Commercial Sales Practices (CSP) and Price Reductions Clause (PRC) framework. This shift moves the audit focus away from commercial pricing relationships and toward the analysis of federal transaction data.

Under the new system, the scope of audits has changed significantly. For contracts participating in TDR, the GSA Office of Inspector General no longer reviews CSP disclosures, Basis of Award tracking, or PRC compliance. Instead, audits now focus on areas like prompt payment discounts, Trade Agreements Act compliance, and labor category qualifications.

"Fully implementing TDR will equip our contracting officers with comprehensive data on purchased items and their prices so they can negotiate effectively and serve as uncompromising fiduciaries of taxpayer dollars."

– Josh Gruenbaum, Federal Acquisition Service Commissioner

The financial impact of TDR is already evident. In 2025, GSA reported $20.2 million in annual cost avoidance, and projections suggest this could reach $50 million once mandatory reporting is fully implemented in 2026. Additionally, TDR has eased the burden on contractors, saving an average of 22 labor hours per contract annually by eliminating the need to track Most Favored Customer and Basis of Award pricing relationships.

TDR vs. CSP: What’s Different

The move from CSP to TDR has fundamentally changed how contractors report sales data, a critical adjustment for small businesses preparing for audits in 2026.

| Feature | Traditional CSP/PRC Model | Transactional Data Reporting (TDR) |

|---|---|---|

| Reporting Frequency | Quarterly | Monthly |

| Administrative Workload | High (tracking MFC/BOA relationships) | Lower (average 22 hours saved/year) |

| Data Detail | Summary sales per SIN | Line-item detail (11+ data points) |

| Pricing Benchmark | Most Favored Customer (MFC) | Market-based "Prices Paid" data |

| Audit Focus | CSP/BOA/PRC Compliance | Transactional accuracy & TAA |

This shift has immediate operational implications for contractors. Reporting has transitioned from quarterly to monthly, streamlining data analysis and reducing the complexity of pricing comparisons. Monthly reports are due within 30 calendar days after the end of each month. Unlike the CSP model, where contractors had to maintain detailed pricing records to prove government pricing was equal to or better than their best commercial customers, TDR eliminates this requirement. Auditors now focus on market-based transactional data instead.

How TDR Improves Data Visibility

TDR enhances audit transparency by requiring monthly reporting of 12 mandatory and 4 optional data points. For products, required fields include Contract/BPA Number, Delivery/Task Order Number, SIN, Description, Manufacturer Name, Manufacturer Part Number, Unit Measure, Quantity, UPC, Price Paid Per Unit, Total Price, and Non-Federal Entity. For services, auditors review fields such as the description of the deliverable, unit of measure, quantity, and price paid per unit.

This detailed transaction-level data replaces the aggregate quarterly reporting of the CSP model. Instead of summary sales figures by SIN, auditors can now analyze pricing patterns across individual transactions. This granular data allows for better monitoring of pricing compliance, location-specific analysis, and review of cycle times. With TDR, GSA gains a clearer view of actual rates charged to government customers, moving beyond reliance on ceiling rates.

"This program mirrors what the private sector is already doing, and will lead to smarter purchasing, helping us streamline procurement."

– Edward C. Forst, GSA Administrator

For small businesses, this enhanced visibility is a double-edged sword. On one hand, accurate reporting minimizes data gaps and reduces follow-up questions from auditors. On the other hand, any inconsistencies in pricing or discount applications become immediately apparent. This level of transparency helps contractors avoid common audit triggers but also demands meticulous attention to detail. Ensuring consistent item setups and discount applications is essential to avoid discrepancies that might draw auditor scrutiny.

One frequent compliance issue is zero-sales reporting. Contractors must submit a report even during months with no sales activity to remain compliant. Missing these reports can still attract audit scrutiny. To address this, small businesses should establish a disciplined monthly close process with internal deadlines to verify and aggregate sales data before the 30-day GSA deadline. Accurate and consistent reporting is now more critical than ever for navigating the evolving audit landscape.

Pricing Compliance and What Auditors Review

The introduction of TDR has reshaped how transaction data is shared with the GSA, but pricing compliance remains a key focus for auditors, especially for contracts still under the traditional Commercial Sales Practices (CSP) model. With some contracts adhering to CSP and others transitioning to TDR, understanding these compliance requirements is essential. Auditors are paying close attention to how contractors justify their GSA pricing, maintain discount relationships, and document price changes. Following the February 2026 OIG report on price variability, contractors are now required to provide detailed pricing justifications for all MAS awards.

"Contractors now face requests for detailed pricing justifications on all MAS awards."

– Gov Contract Pros

In 2026, contractors face a dual audit environment: some operate under the legacy CSP/Price Reduction Clause (PRC) framework, while others have adopted TDR. Knowing which model applies to your contract is critical, as it determines the audit focus and the required documentation. For those still under CSP, traditional compliance elements such as Basis of Award alignment, PRC monitoring, and adherence to EPA clauses remain key areas of scrutiny.

Basis of Award (BOA) and Pricing Practices

Traditional pricing models demand thorough documentation, and auditors are particularly focused on the Basis of Award (BOA) relationship. The BOA identifies the benchmark customer or customer category – often referred to as the "Most Favored Customer" – used to establish the government’s discount. Auditors ensure that the government’s pricing remains equal to or better than what is offered to this benchmark customer throughout the contract.

Compliance issues often arise when contractors fail to update their CSP disclosures to reflect changes in commercial discounting practices. For instance, if price updates or discount structures deviate from the original BOA disclosure without a formal contract modification, auditors will flag these inconsistencies. Similarly, failing to notify the GSA about changes in discounts offered to the Most Favored Customer category can lead to non-compliance findings.

The Price Reduction Clause (PRC) adds another layer of complexity. Contractors must monitor their commercial discount relationships and ensure that if a commercial customer receives more favorable terms than the government, the same improved terms are extended to the government or the contract is formally modified. Auditors closely examine PRC monitoring logs and price comparison sheets to confirm compliance. Missing or incomplete records in these areas often result in deeper audit scrutiny and potential findings of non-compliance.

| Audit Element | Scrutiny Focus in 2026 | Documentation Required |

|---|---|---|

| BOA Alignment | Consistency between CSP and actual sales | Commercial invoices, CSP-1 disclosure |

| PRC Compliance | Monitoring of benchmark customer discounts | PRC monitoring log, price comparison sheets |

| Price Variability | Justification for price differences across agencies | Market research, independent price evaluations |

| EPA Requests | Alignment with authorized EPA clauses | Commercial price lists, index-based justifications |

| Data Accuracy | SKU and Unit of Measure (UOM) consistency | Master Price List, GSA Advantage snapshots |

The FY26 National Defense Authorization Act (NDAA) marks a shift from focusing on the "lowest overall cost alternative" to emphasizing "best value" for MAS contracts. While this change may eventually lead to the retirement of the PRC, contractors under the traditional model must continue to maintain detailed documentation to demonstrate compliance with BOA and PRC requirements.

Economic Price Adjustment (EPA) Clause Requirements

Economic Price Adjustment (EPA) clauses allow contractors to request price changes based on specific triggers outlined in their contracts. As of MAS Refresh 29 in September 2025, the new standard EPA clause GSAR 552.238-120 replaced older clauses like I-FSS-969 and 552.216-70. To incorporate the new EPA method, contractors must submit a "Revise T&C" modification before making any pricing-related changes, such as increases, additions, or option exercises.

Compliance with EPA clauses requires contractors to define both a Method (timing and frequency of adjustments) and a Mechanism (basis for the change, such as a fixed percentage or market index). Auditors ensure that EPA requests align precisely with the contract’s specific clause language. Requests based on general inflation or internal cost increases are typically rejected in favor of those tied directly to authorized EPA triggers.

| EPA Structure | Basis for Increase | Common Failure Point |

|---|---|---|

| Commercial Price List | Formal increase in commercial catalog | Selective price updates inconsistent with Most Favored Customer pricing |

| Market Indicator | Changes in specific indices (e.g., CPI) | Using the wrong CPI series or miscalculating the adjustment period |

| Fixed Escalation | Passage of time (predetermined annual %) | Missing the escalation window or attempting to recover increases retroactively |

EPA modification reviews now take 45–60+ days, creating challenges for contractors trying to align their GSA pricing with commercial market changes. Ray Smith, Founder of Smith Government Consulting, advises: "Submitting too late can leave vendors absorbing increased costs for weeks or months". To reduce delays, contractors should request manufacturer price lists 30 days before they take effect and submit EPA requests as early as possible.

A concerning trend in 2026 involves delays caused by mismatched contractor adjustments. Contracting Officers sometimes refuse to approve an EPA increase until similar increases for other contractors have been processed, resulting in a stalemate based on flawed comparison data. Reviewing the Compliance & Pricing (C&P) report in the Federal Contracting Platform (FCP) before submitting a modification can help contractors anticipate potential issues.

For temporary or minor price reductions, consider using a Temporary Price Reduction (TPR) instead of pursuing a formal EPA decrease. TPRs take effect immediately upon submission in the FCP, bypassing lengthy review timelines. This option allows contractors to respond quickly to market shifts without triggering formal EPA review processes.

Although MAS Refresh 29 has eased restrictions on EPA requests by removing fixed limits and mandatory waiting periods between submissions, meticulous documentation remains essential. Auditors still require detailed justifications that align with the specific EPA method outlined in the contract. Whether using commercial price lists, index-based justifications, or negotiated fixed escalation caps, contractors must ensure their documentation matches the clause language to avoid audit findings. These requirements highlight the importance of precise, contract-based pricing documentation in navigating GSA audits effectively.

What Triggers Audits and How to Maintain Records

Understanding what sparks audits and keeping thorough documentation can help small businesses avoid compliance headaches. Auditors don’t pick contracts at random – they focus on specific warning signs like pricing inconsistencies, reporting errors, and administrative missteps.

Common Audit Triggers

Certain patterns are more likely to attract auditor scrutiny in 2026. A key trigger is pricing discrepancies – especially when government pricing ends up higher than commercial pricing for similar terms or quantities. Auditors carefully check that pricing records align with the Basis of Award (BOA) requirements.

Another red flag? Delayed contract updates. Late Economic Price Adjustment (EPA) justifications or outdated discount structures can raise concerns. Similarly, reporting issues – like missing quarterly sales reports, incomplete Transactional Data Reporting (TDR) submissions, or large gaps between reported and actual sales – signal potential problems. Even administrative oversights, such as overdue Mass Modifications or expired SAM.gov registrations, can prompt an audit.

By understanding these triggers, contractors can better prepare the right documentation to address potential concerns.

Required Documentation for Audits

When audits are triggered, contractors must provide detailed, accurate records to prove compliance. Here’s what auditors typically require:

- Master Price List: This should include SINs, SKUs, GSA prices, units, discounts, and Country of Origin details, updated with every approved modification.

- Transactional Records: Keep quotes, purchase orders, invoices, and delivery confirmations organized throughout the contract term and for three years afterward.

- Commercial Sales Practices (CSP) Documentation: For those under CSP, maintain records that confirm compliance with Most Favored Customer (MFC) terms and BOA alignment. This includes commercial invoices showing pricing and discount terms.

For EPA justifications, provide cost-based evidence such as supplier notices, market index data, or wage index figures. If your contract includes labor categories, you’ll also need resumes and certifications to show compliance with labor requirements.

Trade Agreements Act compliance is another critical area. This means maintaining updated Country of Origin certificates from vendors and documentation proving "substantial transformation" for products from non-designated countries. Meanwhile, cybersecurity audits require an up-to-date System Security Plan (SSP) and Plan of Action and Milestones (POA&M), in line with NIST SP 800‑171 guidelines.

Lastly, don’t overlook administrative records, such as signed SF‑30 forms for contract modifications, current SAM.gov registration details, and proof of Industrial Funding Fee payments.

Centralizing all these records in a digital repository with clear version control and change logs can simplify audit preparation. This organized approach not only speeds up responses but also demonstrates operational discipline, reducing the risk of prolonged audits or negative findings.

How Small Businesses Can Prepare for 2026 GSA Audits

Small businesses face unique challenges when it comes to navigating GSA audits. Instead of scrambling to react when an audit notice arrives, it’s crucial to make compliance a part of your daily operations. Why? Because in 2026, failing to meet compliance standards could result in something as serious as losing your GSA contract. Taking proactive steps now can help safeguard your business from these risks.

Here’s what you need to know – and do – to stay audit-ready.

Steps to Get Audit Ready

Meeting compliance deadlines isn’t optional; it’s mandatory. Missing them could trigger an audit or worse. Here are some key actions to prioritize:

- Catalog updates: Submit updates within 30 days using the Federal Catalog Platform (FCP) or GSA Advantage!.

- Mass Modifications: Accept these within 90 days through eMod to stay current.

- Sales and IFF reporting: File quarterly reports via the Sales Reporting Portal to avoid penalties.

- TAA verification: Conduct quarterly checks to ensure compliance with Trade Agreements Act requirements.

Don’t forget to refresh your price list every six months through FCP and notify your Contracting Officer within 15 days if there’s any change to your Basis of Award discount. Keeping up with accurate monthly TDR submissions is another critical element of staying compliant.

By sticking to these deadlines and processes, you’ll establish a solid foundation for audit readiness. Combine this with professional guidance, and you’ll significantly reduce the chances of triggering an audit.

Getting Expert Help with Compliance

Let’s face it: most small businesses don’t have the resources to maintain a dedicated compliance team. That’s where GSA Focus steps in. They provide full-service support tailored specifically to small businesses working with GSA Schedule contracts.

Here’s what they offer:

- Document preparation: They’ll organize everything auditors might ask for.

- Timely modifications: Ensuring all submissions are accurate and on schedule.

- Compliance management: From pricing policies to TAA requirements, they’ve got it covered.

With a 98% success rate and a refund guarantee, GSA Focus has earned a solid reputation for helping small businesses navigate federal contracting. Whether you’re gearing up for your first audit or trying to keep pace with stricter compliance rules in 2026, expert support could be the key to protecting your contract and avoiding costly mistakes.

For small businesses, the stakes are high, but the right preparation and help can make all the difference.

Conclusion

By 2026, GSA price list audits have reached a new level of complexity. With the expansion of Transactional Data Reporting (TDR) to cover more Special Item Numbers and the simultaneous operation of dual compliance models, small businesses are navigating a more demanding compliance environment than ever before. Adding to the pressure, the administration’s push to cut costs and cancel contracts that fail to meet sales or compliance thresholds highlights the critical need for businesses to stay on top of their obligations.

The key to thriving in this challenging landscape? Preparation. Being ready beats reacting. Auditors aren’t out to catch mistakes – they’re checking that your pricing aligns with the terms of your contract. As Kyle Hayes from USFCR aptly says: "Pricing compliance issues rarely start with bad intent. They start with assumption". This underscores the importance of keeping accurate records, meeting deadlines, and understanding what can trigger an audit.

For small businesses, treating compliance as a regular part of operations can make all the difference. Staying organized with documentation and submitting TDR reports on time are essential steps to safeguard your GSA contract.

Feeling overwhelmed? You’re not alone. Many small businesses lack dedicated compliance teams, which is where expert guidance can make a world of difference. GSA Focus provides personalized support, from document preparation to timely contract modifications and ongoing compliance management, so you can keep your contract intact without the constant worry.

The federal marketplace continues to evolve, but it remains open to small businesses that know the rules and stay ahead of compliance demands. Take action now, and you’ll be ready to tackle whatever 2026 has in store.

FAQs

How do I know if my contract is under TDR or CSP?

To determine whether your contract falls under TDR or CSP, take a close look at the clauses and reporting requirements outlined in your agreement.

- TDR contracts include mandatory Transaction Data Reporting and may have certain clauses removed after the effective date.

- CSP contracts operate with a different approach to pricing and reporting protocols.

Check your contract documents carefully to identify which category applies to your agreement.

What are the biggest TDR reporting mistakes that trigger audits?

When it comes to TDR (Transaction Data Reporting), even small mistakes can lead to big problems. Some of the most frequent issues that raise red flags during audits include:

- Inaccurate sales reporting: Misreporting sales figures can distort the overall data, leading to discrepancies that auditors are quick to notice.

- Misclassification of sales: Categorizing sales incorrectly may seem minor, but it can create confusion and compliance risks.

- Failure to maintain precise transactional data: Without detailed, accurate records of transactions, proving compliance becomes an uphill battle.

These errors not only complicate audits but can also result in significant compliance challenges. The solution? Prioritize accuracy and maintain thorough records to stay on the right side of reporting requirements.

What documents should I have ready before an OIG audit notice?

Before an OIG audit notice lands on your desk, it’s critical to have certain documents ready to go. These include accurate sales records, pricing history, contract compliance documentation, and records proving adherence to price reduction clauses and trade agreement requirements. Staying organized and maintaining up-to-date records isn’t just about convenience – it’s about ensuring a smooth audit process and showing that you’re fully aligned with GSA regulations.

Related Blog Posts

- GSA Pricing Audit Trends: Insights for 2025

- Ultimate Guide to GSA Compliance Standards

- Common GSA Audit Issues and How to Avoid Them

- GSA Modification Documentation: Trends in 2026