When small businesses collaborate under GSA Contractor Team Arrangements (CTAs), profit-sharing becomes a critical factor for success. Unlike traditional prime-subcontractor relationships, CTAs allow each partner to directly contract with the government, making clear profit-sharing agreements essential to avoid disputes and maintain compliance. Here’s what you need to know:

- Understand GSA CTA Rules: Each team member must report their own sales, pay the Industrial Funding Fee (IFF), and follow GSA Schedule pricing rules. CTAs cannot create a joint venture or separate legal entity.

- Define Work Shares: Clearly assign responsibilities and use fixed percentages or dollar amounts to divide tasks and revenue.

- Set Revenue Allocation Terms: Profit must align with each partner’s contributions, especially for small business set-asides.

- Draft Enforceable Agreements: Include clauses for invoicing, payment schedules, dispute resolution, and compliance with GSA regulations.

- Ensure Compliance: Avoid common errors like joint invoicing or conflicting terms with GSA contracts.

Key takeaway: A well-structured profit-sharing agreement not only ensures fairness but also safeguards compliance, making it a cornerstone of successful GSA teaming partnerships.

Teaming Agreement Best Practices for Government Contractors

Understand GSA CTA Regulations on Profit Sharing

Before you dive into drafting profit-sharing terms, it’s critical to get a handle on the rules that govern GSA Contractor Team Arrangements (CTAs). These arrangements operate under specific guidelines that differ from the Federal Acquisition Regulation (FAR).

Key GSA CTA Guidelines

The main regulation for MAS CTAs is GSA Clause I-FSS-40, not FAR Subpart 9.6, which applies to other federal teaming setups. In a CTA, each team member acts as a co-prime contractor and must follow their own MAS contract pricing. Members are also required to report their sales individually and pay the Industrial Funding Fee (IFF) of 0.75% – with no markups allowed on another member’s pricing. This transparency ensures that government buyers see the actual GSA Schedule rates for each team member.

Each team member is also responsible for tracking and reporting their sales and paying the IFF. Federal Schedules, Inc. explains this clearly:

Each Team Member is responsible for tracking and reporting its own sales in accordance with the terms and conditions of the GSA MAS Contract and for paying the related IFF.

If your CTA agreement includes shared incentives or administrative fees, these amounts must not be reported as MAS sales or factored into IFF calculations. For instance, if the team lead charges an administrative fee for coordination, this fee should remain internal and not be reported as government sales. Additionally, for small business set-asides, small business team members must handle at least 50% of the work to comply with FAR 52.219-14.

Following these rules is essential to maintain the regulatory standing of your CTA.

Common Compliance Mistakes to Avoid

Even with clear rules, teams often stumble into compliance issues. Here are some common mistakes – and how to sidestep them.

One major misstep is treating a CTA like a joint venture by forming a new legal entity or subsidiary. Each team member must operate as an independent contractor. Federal Schedules, Inc. underscores this point:

The CTA document must not create a joint venture or separate subsidiary. Each Team Member is operating as a ‘prime’ for the portion of work they are performing.

Invoicing errors are another frequent issue. GSA advises against having the lead contractor invoice the government on behalf of all team members. Instead, each member should handle their own invoicing to ensure proper tracking and IFF reporting. As noted by the Office Manager at FedContractPros:

GSA advises against structuring CTAs in a way where the lead contractor invoices the government on behalf of all team members. Instead, each team member should invoice separately to ensure transparency and compliance.

Other pitfalls include replacing a team member without getting ordering activity approval after an order has been received or drafting CTA terms that conflict with the MAS contract. TurboGSA highlights that when conflicts arise, the GSA MAS Contract always takes precedence. This means profit-sharing terms cannot override pricing, reporting, or other requirements outlined in each member’s GSA Schedule contract.

Select Partners with Aligned Financial Interests

Picking the right partner for your GSA CTA isn’t just about technical skills – it’s about finding someone whose financial stability and business goals align with yours. A partner struggling financially or pursuing conflicting objectives can jeopardize your agreement and even threaten your GSA Schedule contract.

Evaluating Partner Financial Stability

Start by digging into your potential partner’s financial background. Review their credit reports, intellectual property records, and litigation history to spot any red flags like financial trouble or ongoing legal disputes. These issues could hinder their ability to fulfill CTA obligations.

Next, check their compliance record with federal contracts. A solid history with GSA reporting requirements and IFF payments is a good indicator that they can handle the administrative responsibilities of a CTA. Also, confirm that each partner is capable of billing the government directly – this ensures financial independence and protects your margins by avoiding reliance on a lead contractor.

Be cautious about financial arrangements that could lead to SBA affiliation. If a larger partner takes too much control or your business becomes financially dependent on them, you might lose your small business set-aside eligibility. This is especially critical when pursuing contracts designated for small businesses.

Once financial stability is confirmed, shift your focus to whether the partner aligns with your operational and profit-sharing goals.

Ensuring Mutual Goals and Contributions

A successful partnership requires shared objectives and proportional contributions. Define each partner’s responsibilities in detail, using specific percentages or dollar amounts. For instance, instead of vaguely assigning IT services to "Partner A", outline their role explicitly: "Partner A will execute 40% of the work, focusing on network security and cloud migration deliverables."

Profit-sharing should also reflect each partner’s contributions. For SBA-regulated agreements, the small business participant must receive profits that match or exceed the percentage of work they perform. Clearly define roles, including labor categories and deliverables, to avoid confusion or overlap. Address proposal preparation costs upfront by deciding who will cover which portions of the bid and how expenses will be divided before committing resources.

To safeguard the partnership, include dispute resolution procedures in your agreement. This ensures disagreements over contributions or payments don’t spiral into larger issues. Set performance benchmarks that allow for termination if a partner fails to meet their obligations, and limit exclusivity clauses to specific opportunities with defined expiration dates to keep everyone engaged.

Define Work Shares and Revenue Allocation

Once you’ve found the right partner, the next step is dividing responsibilities and deciding how revenue will flow between parties. Clarity is key – assign specific duties to each partner rather than relying on vague descriptions.

Breaking Down Work Shares

To ensure smooth collaboration, assign clear technical areas, labor categories, and deliverables to each partner. In a Contractor Team Arrangement (CTA), each partner maintains its own government contract for its designated scope. This means each partner is individually responsible for meeting their contract obligations, handling sales reporting, and paying their Industrial Funding Fee (IFF).

When dividing work shares, use fixed percentages or dollar amounts. For example, instead of broadly stating, "Partner A handles cybersecurity", outline specific responsibilities like conducting network security assessments, performing vulnerability testing, and managing incident response services.

For small business service contracts, the prime contractor must cover at least 50% of the personnel costs with its own employees to avoid Small Business Administration (SBA) affiliation issues. In SBA-approved mentor-protégé joint ventures or socioeconomic set-asides (such as 8(a), WOSB, HUBZone, or SDVOSB), the small business partner must perform at least 40% of the joint venture’s work. Finalize the subcontract or scope of work during the proposal phase and include it as an exhibit in the teaming agreement. Use mandatory language like "the prime shall award" instead of vague terms like "will negotiate" to avoid creating an unenforceable "agreement to agree".

Once work shares are clearly outlined, the next step is to determine how revenue will be allocated in a way that matches these responsibilities.

Setting Revenue Allocation Terms

Revenue allocation should reflect each partner’s work share and contributions. Under SBA rules, the small business partner in a joint venture must receive profits proportionate to the work they perform – or an even higher percentage if agreed upon. As the SBA regulations explain:

"The small business participant(s) must receive profits from the joint venture commensurate with the work performed by them, or a percentage agreed to by the parties to the joint venture whereby the small business participant(s) receive profits from the joint venture that exceed the percentage commensurate with the work performed by them."

Define whether revenue allocation will be based on total contract dollars, labor costs, or other specific metrics. Contracts expert Kathy Wright emphasizes the importance of clarity: "If the baseline is not defined in the Teaming Agreement, it is open to interpretation". This lack of precision can lead to disputes, especially when cumulative task order values don’t align with the promised percentages.

To avoid confusion, calculate the "addressable workshare" by excluding the prime’s project management costs, profit, and burdens tied to subcontractor rates – these belong to the prime. Clearly spell out how project management fees, award fees, or incentive fees will be divided among team members. Avoid using terms like "targeted", "approximate", or "estimated" when defining work shares. Firm commitments are essential to prevent disagreements during execution.

Draft Profit-Sharing Terms in the CTA Agreement

Turning your profit-sharing terms into a clear, enforceable contract is essential for ensuring compliance with GSA regulations and protecting all parties involved. This section focuses on formalizing those agreements and laying out the terms in a way that leaves no room for ambiguity.

Key Clauses to Include

When drafting your CTA agreement, make sure to include these critical clauses:

Party identification: Clearly list the full names, addresses, and GSA MAS contract numbers of all team members. This ensures that everyone involved holds a valid GSA Schedule.

Invoicing and payment designation: Decide which team member will handle invoicing. While GSA recommends individual invoicing for transparency, you can designate a lead to coordinate invoicing as long as each member’s GSA price is maintained. Be specific about payment schedules – e.g., “within 30 days after the end of each calendar quarter” – and include terms for late payments, such as interest rates.

Pricing and rate calculation: Lay out unit prices or hourly rates, explain the basis for these calculations, and confirm that all rates are at or below each contractor’s GSA MAS Contract prices. Also, specify how any order-level incentives or fees will be shared.

Profit definition and reporting: Define “profit” as revenue minus allowable expenses. Require electronic revenue-sharing reports on a quarterly and annual basis, even during periods when no profit is due.

Audit and record-keeping: Ensure all team members maintain GAAP-compliant records, which will be subject to audit to verify the accuracy of profit-sharing.

Dispute resolution: Specify that any disputes over payment or profit-sharing will be resolved internally, without involving the government. Federal Schedules, Inc. advises:

The CTA Agreement should acknowledge that the Team Members, without any involvement by the government, would resolve any dispute involving the distribution of payment between the Team Leader and the Team Members.

Mandatory language: Use definitive terms in the contract. For example, say, “the lead shall award the subcontract,” instead of vague phrases like “will negotiate,” to avoid creating an unenforceable agreement.

These clauses form the backbone of a well-structured agreement that complies with regulations and protects all parties.

Ensuring Legal and Regulatory Compliance

Profit-sharing terms must align with GSA regulations and federal contracting guidelines. The CTA document should explicitly state that all team members remain independent contractors and that the agreement does not create a joint venture or separate legal entity. Federal Schedules, Inc. highlights:

The CTA document must not create a joint venture or separate subsidiary. Each Team Member is operating as a ‘prime’ for the portion of work they are performing.

Include a precedence clause to address potential conflicts. This clause should state that, in the event of a conflict between the CTA agreement and any member’s GSA MAS Contract, the GSA MAS Contract takes precedence.

For small business set-asides, ensure your agreement reflects that small businesses must perform at least 50% of the work, as required by FAR 52.219-14. Additionally, account for the GSA Industrial Funding Fee (IFF), which is typically 0.75% of the total sales price.

Clarify under whose name the government will evaluate performance in the Contractor Performance Assessment Reporting System (CPARS). Finally, include termination provisions that specify conditions for ending the agreement, such as the loss of an award or the execution of a formal subcontract. To strengthen legal protection, negotiate full subcontract terms before proposal submission and attach these as an exhibit to the teaming agreement.

Once your profit-sharing terms are documented and compliant, the next step is implementing invoicing procedures and IFF reporting to ensure the agreement works seamlessly in practice.

Implement Invoicing, Payment Distribution, and IFF Reporting

Once profit-sharing terms and compliance clauses are in place, it’s time to bring them to life through actionable processes. This means setting up efficient invoicing systems, handling payment distribution, and meeting Industrial Funding Fee (IFF) reporting requirements. A well-executed system avoids delays and ensures compliance.

Streamlining Invoicing Processes

The Contractor Teaming Arrangement (CTA) must clearly identify who is responsible for invoicing. According to GSA guidelines, the government is encouraged to pay each team member directly. This approach reduces administrative work for the team lead and ensures payments are distributed promptly. TurboGSA elaborates:

While the team lead may submit an invoice on behalf of all team members, GSA recommends that payment be made to each team member.

However, the CTA can also allow for a team lead to manage payment distribution. Whichever method you choose, consistency in invoice formatting is crucial. Each invoice should include the following details for smooth processing:

- GSA Contract Number

- DUNS/UEI Number

- Special Item Number (SIN)

- Part Number or Service Description

Additionally, any discounts should be clearly listed on quotes, proposals, and invoices to avoid retroactive adjustments. For items not covered under the GSA Schedule, make sure they’re labeled as "Open Market" to prevent IFF miscalculations. Isabel Sabie, Contract Administrator at Winvale, advises:

If you include Open Market items on a GSA order, make sure you mark the items as Open Market to avoid overpaying the IFF fee.

It’s also worth noting that disputes over payment distribution must be resolved internally among team members, as the government does not mediate such conflicts.

By following these invoicing practices, you’ll set the stage for accurate and efficient IFF reporting.

Managing IFF Reporting Responsibilities

Every team member is responsible for tracking their own sales and paying the Industrial Funding Fee (IFF). The IFF rate is currently 0.75% of GSA sales. This fee applies to the base price and any additional charges but excludes state/local taxes and shipping fees if itemized separately. Contractors must submit their sales reports through the FAS Sales Reporting Portal. The reporting schedule depends on whether you fall under Transactional Data Reporting (TDR):

- TDR Contractors: Report sales monthly.

- Non-TDR Contractors: Report sales quarterly.

Regardless of sales volume, contractors must file a "zero sales" report if no sales occur during the reporting period. Reports and IFF payments are due 30 calendar days after the end of each quarter – January 30, April 30, July 30, and October 30.

To ensure compliance, record sales consistently – either at the time of invoicing or payment – so all team members report in sync. GSA allows sales to be recorded in line with your commercial accounting practices. To simplify reporting, consider tracking sales by SIN, as this aligns with the portal’s requirements.

| Reporting Type | Frequency | Data Required | IFF Payment Deadline |

|---|---|---|---|

| Non-TDR Contractors | Quarterly | Total dollar amount per SIN | 30 days after quarter end |

| TDR Contractors | Monthly | PO#, Unit Cost, Quantity, Customer Type | 30 days after quarter end |

With invoicing and IFF reporting systems in place, your team is equipped to manage financial operations effectively. Up next, we’ll delve into how profit-sharing models differ across GSA partnership structures.

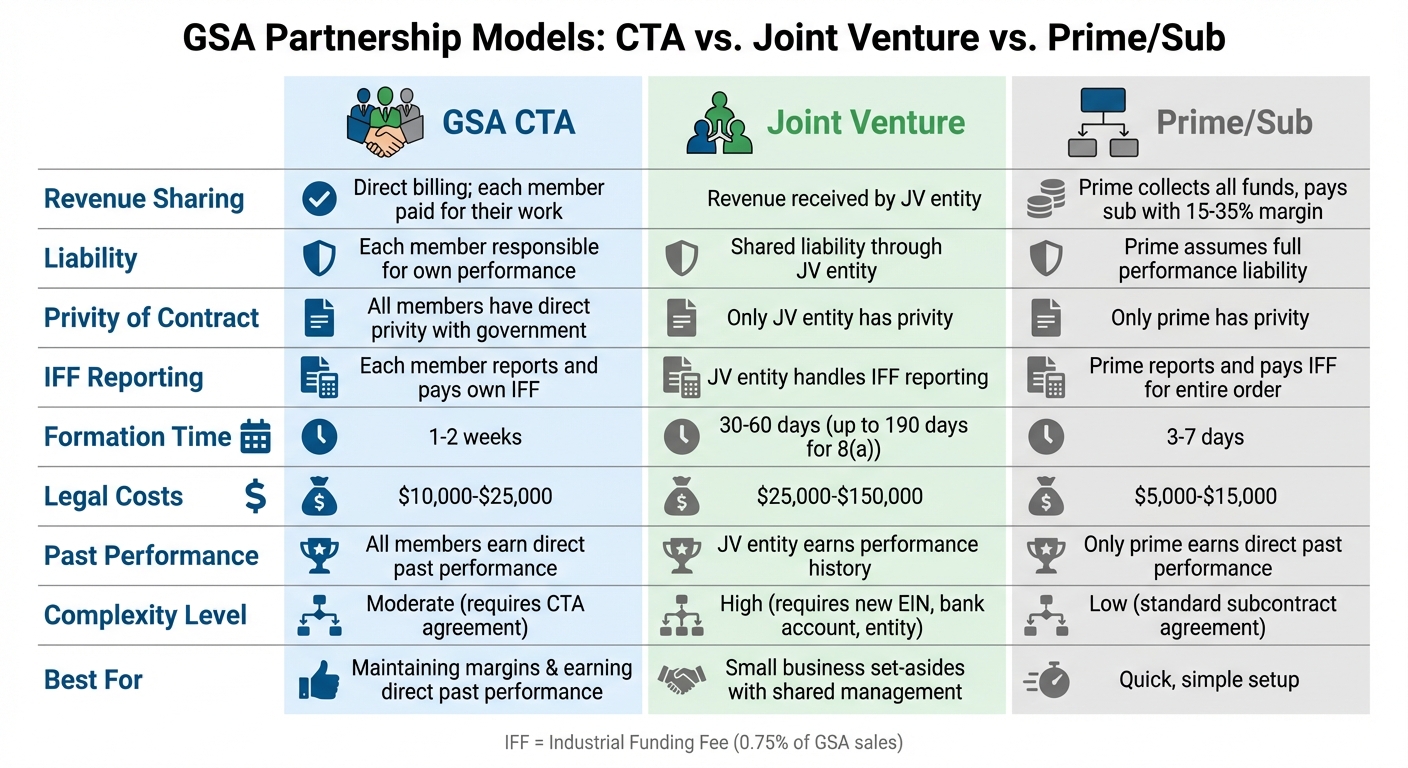

Comparison of Profit Sharing in GSA CTAs, Joint Ventures, and Prime/Sub Relationships

GSA CTA vs Joint Venture vs Prime-Sub: Comparison of Profit Sharing Models

Now that we’ve covered invoicing and IFF reporting, let’s dive into how profit sharing works across Contractor Teaming Arrangements (CTAs), Joint Ventures (JVs), and Prime/Sub relationships. Each structure comes with its own approach to revenue distribution, liability, and administrative tasks.

In a CTA, every member acts as a co-prime, invoicing the government directly at their GSA Schedule rates. Payments go straight to each partner for their specific contributions, with no intermediary involved. Compliance is straightforward – each member tracks their own sales and handles their IFF payments.

For Prime/Sub relationships, all revenue flows through the prime contractor, who is responsible for paying the subcontractor. The prime assumes full liability for the entire project, including the subcontractor’s work. This model is straightforward and quick to set up, with legal costs ranging from $5,000 to $15,000 and a formation timeline of just 3 to 7 days.

Joint Ventures, on the other hand, require forming a completely new legal entity with its own tax ID and bank account. The JV entity collects all revenue and distributes profits based on the partnership agreement. This structure involves shared liability and is the most complex to establish, with legal costs between $25,000 and $150,000 and formation times ranging from 30 to 60 days – or up to 190 days for 8(a) JVs. JVs also need separate SAM registration and can compete for small business set-asides, provided the small business partner handles at least 40% of the work. Compared to CTAs and Prime/Sub models, JVs stand out for their complexity and shared responsibility.

Here’s a quick comparison to help you decide which model fits your needs:

Comparison Table: CTA vs. Joint Venture vs. Prime/Sub

| Feature | GSA CTA | Joint Venture | Prime/Sub |

|---|---|---|---|

| Revenue Sharing | Direct billing; each member is paid for their work | Revenue is received by the JV entity | Prime collects all funds, paying subcontractor with a 15–35% margin |

| Liability | Each member is responsible for their own performance | Shared liability through the JV entity | Prime assumes full performance liability |

| Privity of Contract | All members have direct privity with the government | Only the JV entity has privity | Only the prime has privity |

| IFF Reporting | Each member reports and pays their own IFF | JV entity handles IFF reporting | Prime reports and pays IFF for the entire order |

| Formation Time | 1–2 weeks | 30–60 days (up to 190 days for 8(a)) | 3–7 days |

| Legal Costs | $10,000–$25,000 | $25,000–$150,000 | $5,000–$15,000 |

| Past Performance | All members earn direct past performance | JV entity earns the performance history | Only the prime earns direct past performance |

| Complexity | Moderate; requires a CTA agreement | High; requires new EIN, bank account, and entity | Low; standard subcontract agreement |

- Choose a CTA if maintaining your margins and earning direct past performance are priorities.

- Opt for a Prime/Sub model when you need a quick and simple setup.

- Select a Joint Venture if you’re targeting small business set-asides or prefer shared management and liability.

Conclusion: Key Takeaways for Successful Profit Sharing in GSA Teaming Agreements

Recap of Best Practices

Navigating profit sharing in GSA teaming agreements means focusing on clarity, fairness, and strict adherence to regulations. Start by defining work shares with precise percentages or dollar amounts. As the GovContractFinder Team emphasizes, "Vague work share: Specify work share percentages or dollar amounts rather than general descriptions". Payment terms should also be clearly outlined, covering timing, conditions, and their connection to specific labor categories, technical areas, and deliverables. To safeguard the agreement, include clauses for dispute resolution and termination, ensuring both parties know how to handle potential conflicts or exits. For agreements involving socioeconomic set-asides, remember that the small business partner must handle at least 40% of the work. Staying compliant with SBA and GSA regulations is non-negotiable. By following these guidelines, small businesses can approach GSA teaming agreements with confidence.

Next Steps for Small Businesses

Once you’ve mapped out a clear profit-sharing structure, the next step is securing expert advice to finalize your Contractor Teaming Arrangement (CTA). For those new to GSA contracting – or simply looking for extra assurance – working with professionals who understand federal procurement can make all the difference. GSA Focus offers small businesses end-to-end support, covering everything from document preparation and compliance to negotiation assistance, helping you unlock federal contracting opportunities.

Start by evaluating your potential partner’s financial stability and ensuring your business goals align. Then, draft your agreement with detailed clauses covering work shares, payment terms, dispute resolution, and termination. With a solid structure in place, your teaming arrangement can set the stage for fair profits and long-term success in federal contracting.

FAQs

Can a CTA include a shared profit pool without creating a joint venture?

Yes, a CTA can include a shared profit pool without requiring the formation of a joint venture. In a CTA, participants operate as co-prime contractors, each working under their own individual contracts. Unlike a joint venture, this structure avoids creating a separate legal entity, allowing members to collaborate while retaining their own contractual obligations and responsibilities.

How do we set workshare and profit split for a small business set-aside CTA?

When establishing workshare and profit distribution in a small business set-aside Contract Teaming Agreement (CTA), clarity is key. Define each party’s roles and responsibilities explicitly within the agreement. Profit sharing should reflect ownership stakes, contributions, or the level of effort each party brings to the table, while staying compliant with SBA and GSA regulations.

It’s also important to align the profit distribution with the agreed-upon scope of work and responsibilities for each participant. For added assurance of fairness and regulatory compliance, consider consulting with legal or contracting experts. Their guidance can help navigate the complexities and ensure everything is structured appropriately.

What should we do if the CTA profit terms conflict with a member’s GSA Schedule?

If profit-sharing terms in a call-to-action (CTA) clash with a member’s GSA Schedule, it’s crucial to ensure the arrangement complies with each member’s contractual responsibilities. Carefully review the GSA Schedule terms to prevent any compliance issues. Should conflicts emerge, adjust the terms to align with individual commitments or consult an expert for guidance. Profit-sharing agreements must strictly adhere to the requirements outlined in the member’s GSA Schedule.

Related Blog Posts

- Types of GSA Teaming Agreements Explained

- Ultimate Guide to Teaming Agreements for Small Businesses

- Best Practices for Small Business Teaming Success

- Best Practices for Federal Teaming Success